Home service business owners know how to clean, mow, fix, install, and deliver, but not how to track the numbers that decide if their business lives or dies.

Take a mid-sized HVAC or cleaning company as an example. Jobs keep coming in, the schedule is full, and the owner assumes things are fine. Then payroll hits. Material bills stack up. A commercial client delays payment. Suddenly, cash is tight and no one knows why.

And that’s where the trouble starts. 9 out of 10 home service businesses that fail don’t die from lack of work, they die from financial mismanagement.

Accounting is not a year-end task for your CPA.

It’s a daily system for tracking where money moves, why it moves, and what decisions it should drive.

The job of accounting is simple:

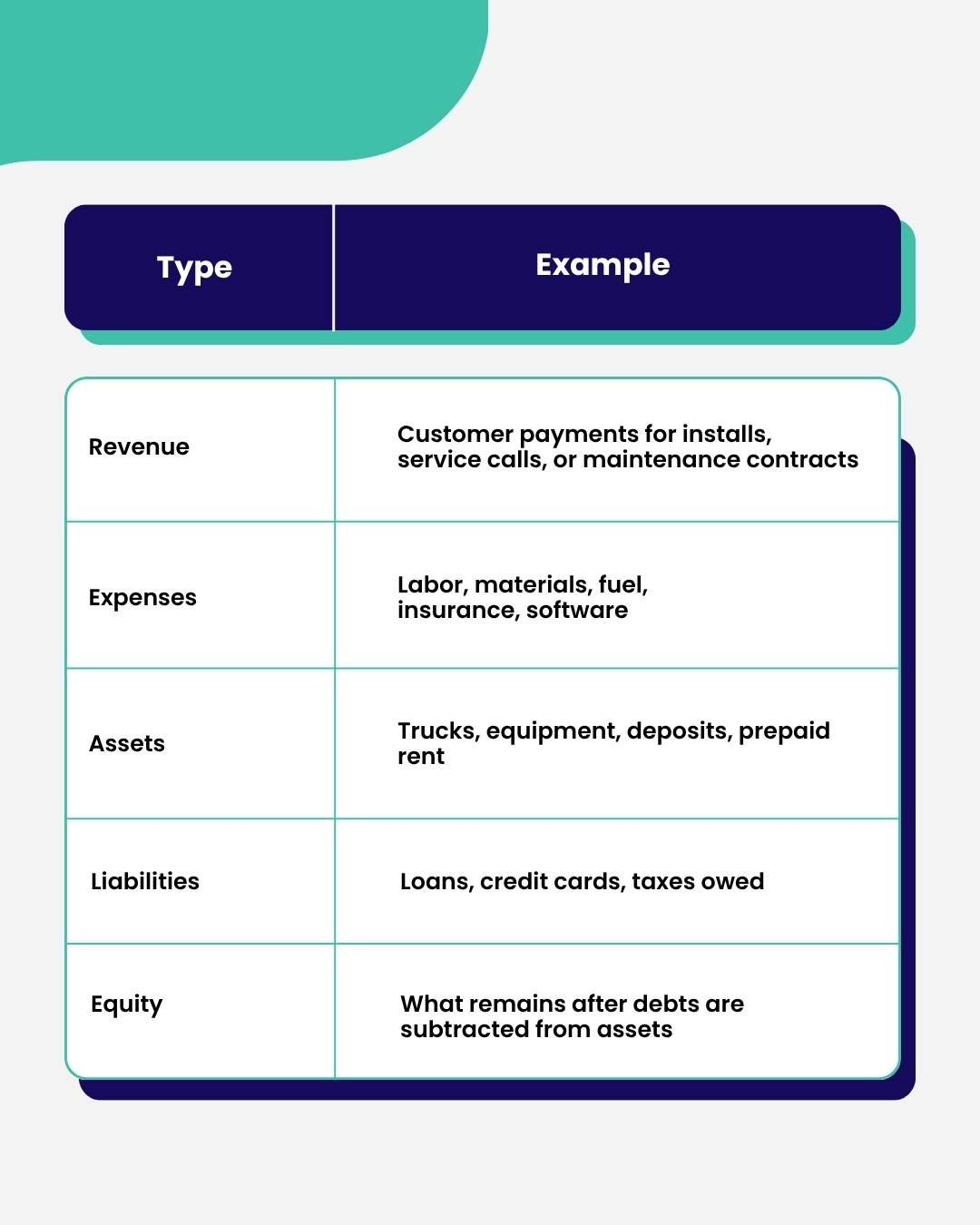

Every home-service company runs on five transaction types:

Sync business bank accounts and credit cards to QuickBooks Online or a similar system.

Create categories by service line, installations, maintenance, and repairs, so each job type can be measured separately.

Accurate classification is what makes reports useful. If a $1,200 materials bill gets coded as “supplies” instead of “cost of goods sold,” gross margin calculations will always be wrong.

a. Income Statement

Shows revenue, cost of goods, operating expenses, and profit.

Focus on these indicators:

b. Balance Sheet

Lists assets, debts, and equity. It tells you whether the business can meet its obligations.

Check monthly:

If trucks and equipment dominate assets but cash is thin, you’re asset-heavy and liquidity-poor. That’s what creates payroll pressure even when profits look fine.

c. Cash-Flow Statement

Tracks all inflows and outflows, including loan payments and owner draws. It explains the disconnect between a profitable month and an empty bank account.

Review it weekly. The first signal of stress always appears here.

Financial reports matter only if they shape actions.

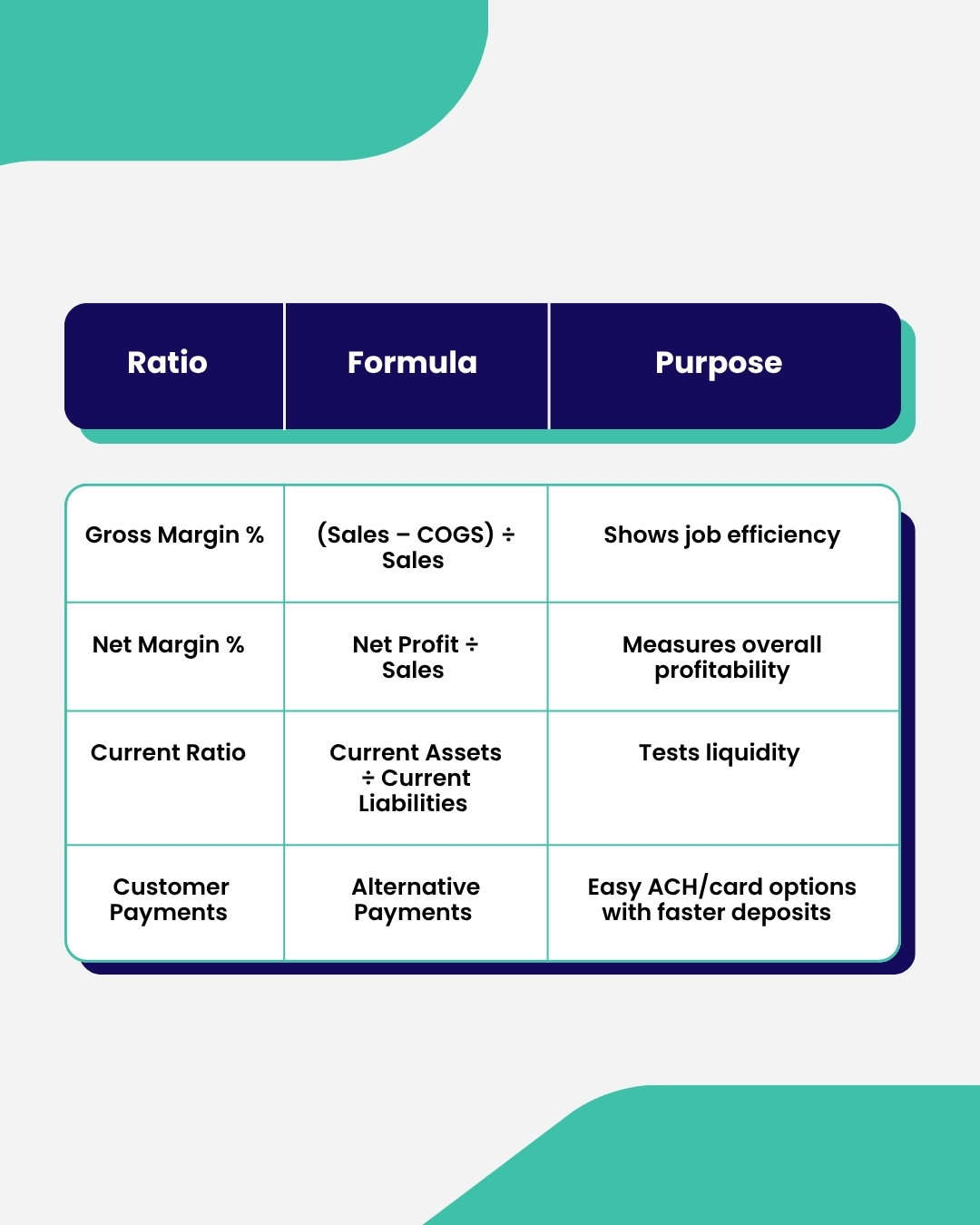

Four basic ratios give almost every answer you need:

Example: if A/R turnover falls below 10x per year, invoices are aging beyond 30 days — you’ll hit a cash gap before tax season.

This data replaces assumptions with measurable indicators of financial health.

Bookkeeping looks backward. A CFO system looks forward.

Here’s what separates the two:

With these tools, financial meetings move from “What happened?” to “What should we do next?”

Home-service businesses often face irregular cash cycles, heavy revenue in summer, slow months in winter. Accounting helps you smooth those swings.

Use these controls:

Predictable cash flow gives you negotiation power with suppliers and better borrowing terms with banks.

Job costing turns accounting data into operational control.

Track every job’s labor, materials, and overhead allocation.

Compare estimated vs. actual margin.

If the target was 50% and the result was 38%, review:

Systematic job costing fixes small leaks before they turn into margin erosion across the season.

Borrowing from Alex Hormozi’s model to home services:

Product + Service + Access = Scalable Business.

Here’s what that looks like in the field:

From an accounting perspective, this model shifts more income to predictable, high-margin categories. It simplifies cash-flow forecasting and increases enterprise value because recurring revenue gets valued higher than project-based work.

Consistency builds accuracy. Accuracy builds confidence in decisions.

When done correctly, accounting gives operators three advantages:

You can borrow confidently. Hire on purpose. And forecast, not fear, the next season. In short, accounting shows whether you can afford growth, not just desire it.

Accounting for home-service businesses is not about taxes or compliance. It’s the financial infrastructure that keeps your company operational and investable.

Do that, and accounting becomes the quiet system that lets your home-service business expand with confidence and stay profitable year-round.

Not sure if your accounting system is working for you?

We help home service owners build accounting systems that track profit, control cash, and plan growth.

Schedule a short review call, and we’ll show you where your books can start driving better decisions.